Analyst Opinion: Neutral

Source: finviz.com

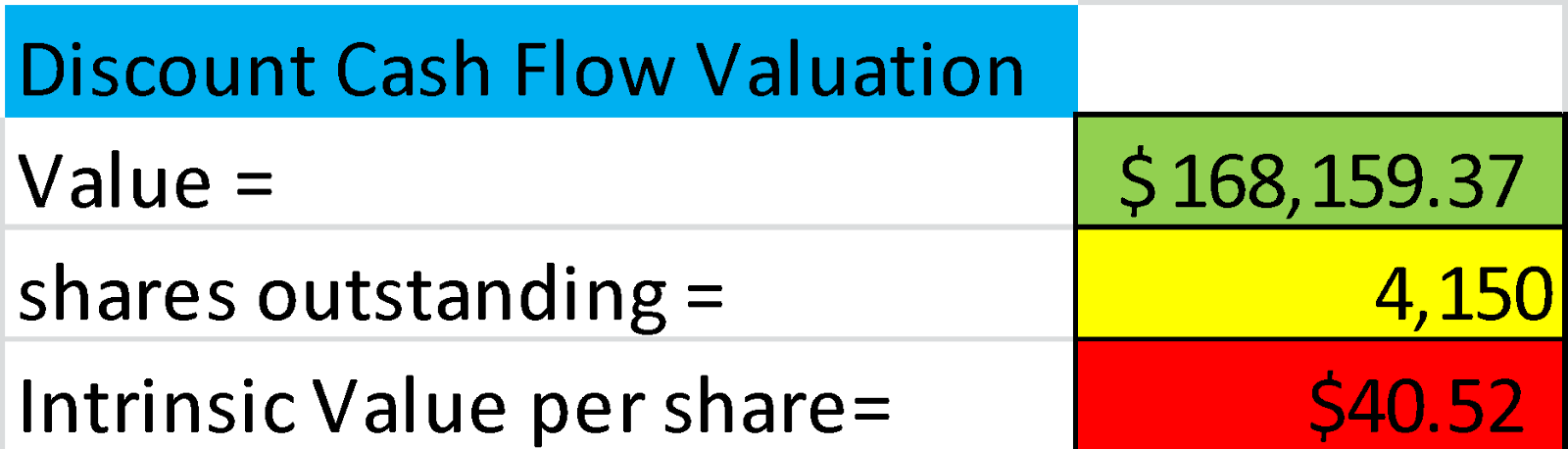

Valuation of Verizon Communications shows the firm to be fairly valued. Although the valuation model showed a rough estimation of $40.52 per share based on future estimates of revenues and earnings growth, Verizon continues to perform very strongly in areas involving network capacity, reliability, and brand strength. Verizon also trades at a price to earnings of approximately 10.5, far below the industry average of 15.96. Verizon has shown signs of better financial management as margins have been strengthening over the past five years. Verizon faces more intense competition which could hurt both future revenues and margins as they drop prices to attract more customers to enter into wireless contracts. FiOS has been a strong growth area for Verizon recently and continues to grow in popularity as it competes with Comcast, DISH, and DirectTV. A strong brand and continued emphasis in improving data capacity and network reliability will continue to be a driving force as Verizon’s position in the communications market as well as the growth and popularity of FiOS.

Verizon Communications is a holding company that is one of the world’s largest and leading providers of communications and information services to consumers, businesses, and governmental agencies. Verizon has two operating segments, Wireless and Wireline. Wireless provides voice and data services and equipment sales on one of the most extensive wireless networks. The wireline segment provides consumer, business, and governments with communications products and services which include broadband data and video services, voice, long distance and other communications products. Verizon emphasizes significant capital investments to maintain network reliability and speed by investing in the fiber optic network that supports their wireless and wireline businesses and by maintaining a significant advanced database capacity.

Company Size

Large company size provides a multitude of benefits. Most notably larger brand equity, access to financial resources, purchasing power for acquisitions, and the possibility to work with large customers such as governments and large corporations

Leader in Network Quality

Verizon Communications invests capital focused on adding capacity to optimize 4G LTE network, primarily by increasing network density. Consistent investment in wireless has led them to become a very strong brand with great customer loyalty. Verizon’s churn (turnover) of postpaid subscribers has stayed low signifying that customers are staying loyal to Verizon. A strong brand name created through network reliability has also insulated Verizon from industry price wars. Verizon has also been focusing on converting from copper to fiber optic cables, providing a higher quality of service and also savings in maintenance and improvements.

Strengthening Margins

Verizon’s margins have been strengthening over the past five years primarily through management’s financial management of operating expenses. Gross margins have been increasing from its level of 58.91% in 2009, to its current level of 62.64% TTM. Net Margin has followed this trend, increasing from its level of 3.39% in 2009 to its current level of 12.50% TTM, a sign of management’s effectiveness in cutting costs, as improvements in gross margins have come as a result of a decreasing SG&A.

High Dividend

High dividend payout of 4.6%

Stable and Increasing Revenues

Brand loyalty and network reliability has created stable and increasing revenues over the past four years. Revenues derived from pricing plans and strong growth from FiOS generates consistently increasing revenues. FiOS revenue has sustained strong double digit growth and now represents 75% of consumer revenue in the wireline operating segment.

Verizon has had an annual growth rate over the past three years of 4.20%. Future revenue growth will be increased through the success of Verizon FiOS which has sustained double digit growth through the past two quarters and continues to be a driving for the company. Revenue growth and strengthening margins has led to an increase in earnings per share from FY2012 to FY2013 of 16%. Verizon has been approved to repurchase as many as 100 million shares over the course of three years, however CFO Fran Shammo has noted that Verizon probably will not repurchase company stock for the next two or three years. Under the previous three-year authorization for 100 million shares which expired last February, Verizon only acquired 3.5 million shares.

Company Size

Large company size also provides some disadvantages. Multiple levels of management reduce the speed of decision making, also difficulties to implement company-wide changes. Errors in products or network immediately create bad publicity among a large customer base.

Increasing Competition

Verizon is facing increasing competition especially from competitor Sprint. Sprint has received awards in network reliability and is a releasing new pricing program targeting the IPhone 6. Sprint’s new aggressive pricing strategies come with the recent appointment of new CEO Marcelo Claure. An increase in postpaid churn was slightly up over the past year around 1%, signifying increasing pressure from competition especially as competing network become more reliable and remains cheaper Verizon may be forced to cut prices, cutting into margins and profitability.

Other competitors include AT&T in wireless communications along with Sprint. Comcast, DirectTV, and Dish compete with Verizon FiOS. FiOS has been competing very effectively, boasting better data speeds, higher reliability, picture quality, and service satisfaction. FiOS has been the main growth catalyst behind Verizon revenue growth, in the wireless segment competitors have a chance to poach customer contracts as the largest amount of contract expire this holiday season, numbering 3.1 million IPhone customers. Sprint has been very aggressive with recent pricing strategies, offering their $60 Unlimited Plan where customers purchase unlimited talk and text for $60 per month/per line.

High Debt Level

Verizon operates with a debt/equity of approximately 60%. This has translated into higher interest payments. Increased competition could start to decrease revenues which would decrease the interest coverage as profit margins start to decline.

Strengths

|

Weaknesses

|

Opportunities

|

Threats

|

Wireless

Verizon is the fastest market share gainer in the wireless communications market. While it remains second to AT&T it has enjoyed much higher growth rates and is likely to outpace their rival. Sprint, while falling drastically in market share in 2013 has a new direction with new company CEO Fran Shammo and pricing plans that target the recent IPhone 6 launch that could regain some of their old market position.

Top Competitors

|

2011 Revenue Share

|

2012 Revenue Share

|

2013 Revenue Share

|

TTM Revenue Share

|

Revenue Growth Rate

|

Verizon

|

30.43%

|

31.79%

|

35.75%

|

36.49%

|

7.44%

|

Sprint

|

14.61%

|

14.81%

|

7.45%

|

7.29%

|

-23.63%

|

AT&T

|

54.96%

|

53.40%

|

56.80%

|

56.23%

|

0.76%

|

Total Market

|

100% = Market revenue 2012

|

100% = Market revenue 2013

|

Market Growth rate = -.076%

|

Wireline

Verizon has been outpaced in the wireless industry over the past 3 years. Comcast still commands the majority of the market and is growing their services of cable, internet, and hardline phone service. However, Verizon has had very successful growth in FiOS over the past two quarters, especially with the release of FiOS Quantum; Verizon could look to take a larger market role in their wireline segment

Top Competitors

|

2011 Revenue Share

|

2012 Revenue Share

|

2013 Revenue Share

|

TTM Revenue Share

|

Revenue Growth Rate

|

Verizon

|

29.52%

|

27.18%

|

26.11%

|

25.34%

|

-1.81%

|

Comcast

|

40.52%

|

42.75%

|

43.04%

|

44.23%

|

7.69%

|

DirectTV

|

19.76%

|

20.32%

|

21.59%

|

21.11%

|

9.15%

|

DISH

|

10.19%

|

9.75%

|

9.26%

|

9.32%

|

-0.49%

|

Total Market

|

100% = Market revenue 2012

|

100% = Market revenue 2013

|

Market Growth rate = 4.43%

|

Despite having a higher cost of sales than other competitors, the profitability of Verizon comes into clear focus with a higher operating and net margin than other competitors in both wireless and wireline industries.

VZ

|

T

|

S

|

CMCSA

|

DTV

| |

Market Cap

|

207.09B

|

178.97B

|

23.67B

|

139.98B

|

42.88B

|

Revenue (TTM)

|

124.95B

|

131.17B

|

34.56B

|

67.97B

|

32.44B

|

Latest Quarter Rev. Growth (yoy)

|

4.32%

|

1.55%

|

-.99%

|

3.96%

|

2.91%

|

Gross Margin (TTM)

|

36.99%

|

59.2%

|

42.12%

|

69.39%

|

47.34%

|

Operating Margin (TTM)

|

24.90%

|

23.26%

|

-5.74%

|

21.72%

|

16.06%

|

Net Margin (TTM)

|

17.40%

|

13.75%

|

-11.01%

|

12.31%

|

8.87%

|

Source: Morningstar, SEC filings

|

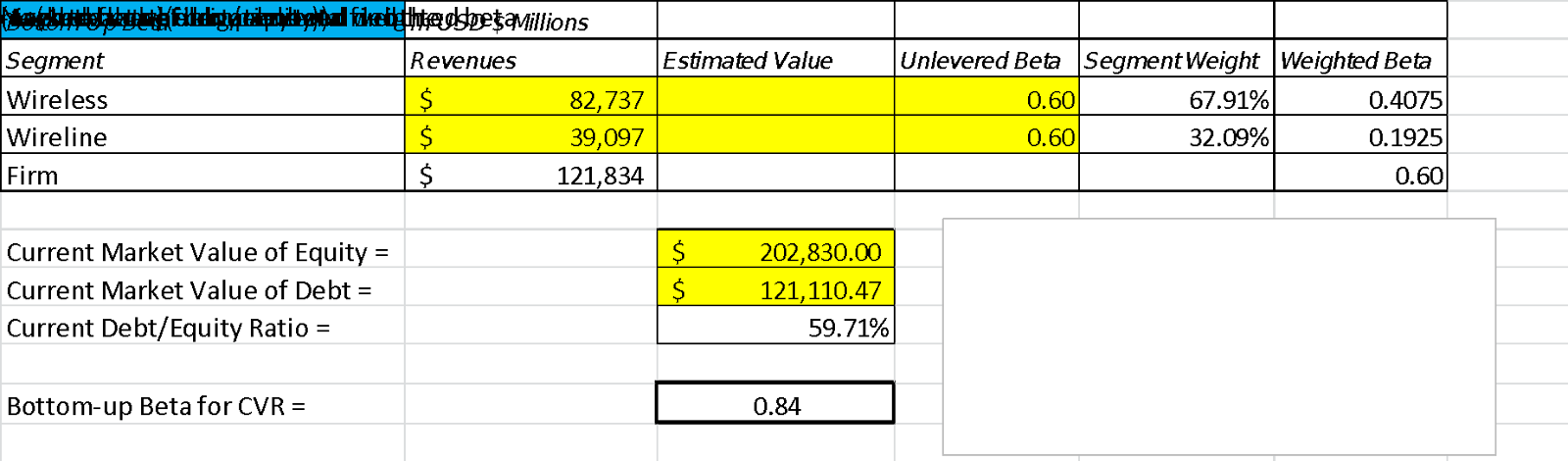

The risk estimation is based on the average beta for the industry that Verizon operates in, being both wireless and wireline communications. The measured beta for Verizon was 0.42, this beta estimation that is based on historical results does not adequately reflect the increasing competition risk and is not adjusted for the firm’s leverage which would inherently increase risk. By adjusting for increased future risk and fully leveraging the beta (including off balance sheet debt obligations such as operating leases), the beta estimation was found to be 0.84. While being double the CAPM beta estimation this new leveraged beta is still below 1 and shows that Verizon is of below average risk.

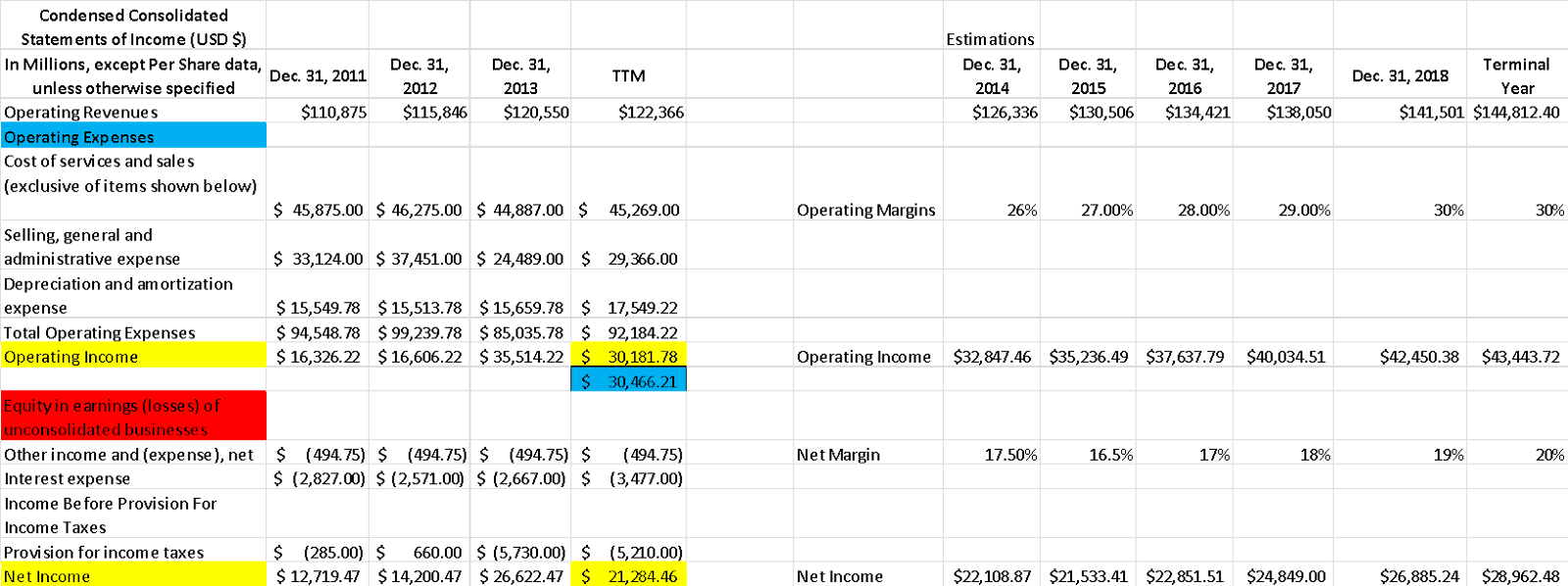

Earnings were adjusted for FY2011 through FY2013. One-time expenses and income such as Equity in earnings of unconsolidated were not included in earnings and earnings projections because these do not reflect the earnings power of Verizon and would be difficult to project into the future. Other income and (expense), net was averaged out over the three year period because it showed volatility over the three year period. Operating expenses were also adjusted to reflect the fact that operating leases were transferred into debt as they fulfil the characteristics of debt. Revenue is estimated to increase 4.80% in 2014 and then decrease to 3.30% in 2015, this is in reflection of the increased competition that could take Verizon’s customers if the wireless communications price war continues to drop prices. Operating margins are expected to strengthen over the next five years to an industry average of 30%, operating margins have been positively trending as a more effective financial management aims at cutting costs. Net margin is expected to decrease from 2014-2015 reflecting increased competition and a growing level of debt. This is estimated to strengthen to an industry average 20% after FY2018.

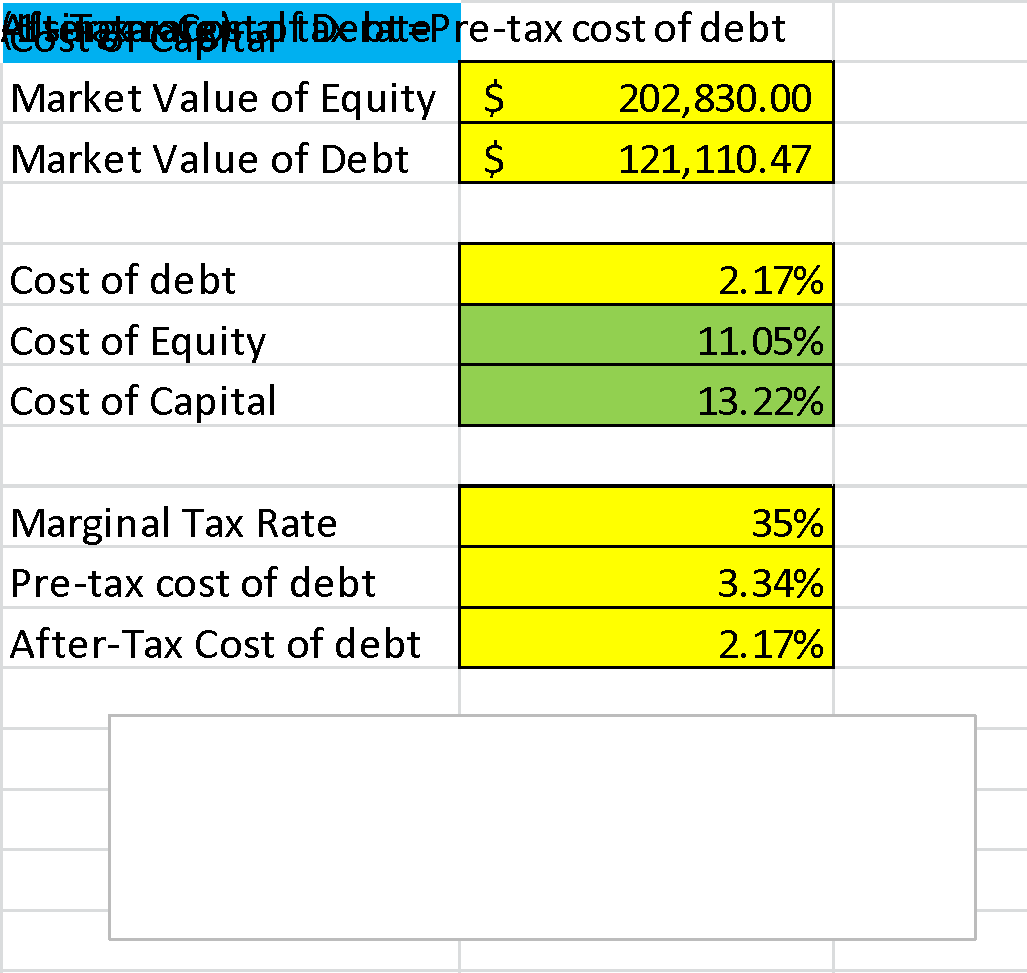

Future estimations of net income were discounted back to present value using an estimated cost of capital for Verizon. Cost of capital was determined by estimating the cost of equity and cost of debt. Cost of equity was computed using the leveraged beta for Verizon and an implied risk premium focusing on expected SP 500 cash flows over the next five years, cost of debt was estimated by using Verizon’s company default spread measured through their Moody’s bonds rating, the interest rate on a 10 year treasury bond, and the marginal tax rate.

After discounting the estimated future net income using the cost of capital the value for Verizon was estimated be approximately $40.52. A discount of approximately 18% from the current trading value.